The Need for Repo Clearing

The Need for Repo Clearing

By Nigel de Jong, RepoClear

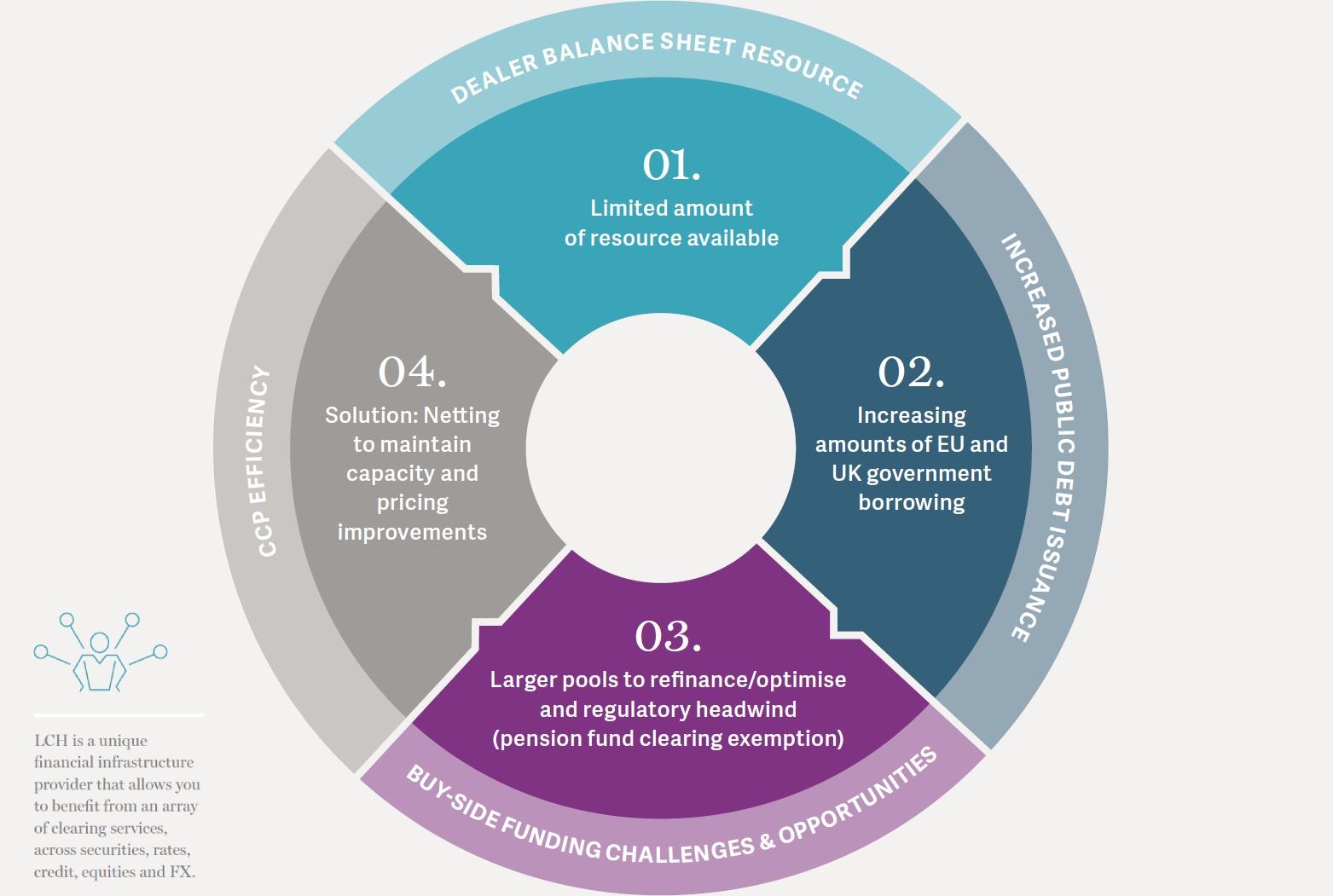

Over the past year or so, it has become evident that repo clearing is essential for achieving efficiency in all market conditions. This is reflected in the growing demand for cleared repo, which, according to EU SFTR data included in the latest ICMA European repo survey, represents around 50% of outstanding loan value of the overall repo market, a trend fuelled in part by concerns highlighted during the COVID-19-driven volatility around access to safe and secure funding. This was especially acute in March 2020, when liquidity was at a premium and secured funding was in demand.

As a result of these stresses, some buy-side firms struggled to access secured repo markets and started to review their toolbox of execution options for when such a crisis repeats itself. This highlighted the ongoing need for repo clearing, not just as a safety net for difficult times, but as a mechanism for achieving better pricing and adequate capacity in both volatile and calm markets.

ENDURING BENEFITS

While recent events have focused attention, the core benefits of repo clearing are enduring. In particular, balance sheet netting helps both sell-side and buy-side market participants by creating capacity that dealers can provide to their clients. Effective balance sheet management is critical; netting reduces risk and frees up capital to finance growing debt in the EU and elsewhere. This includes EU SURE bonds and Next Generation first issuance, which offer vital help for employment schemes throughout the EU, and the growing list of ESG government issuance.

This is good news for users of a service such as LCH RepoClear, which delivers an opportunity for an array of netting benefits that are significantly enhanced by the size of its liquidity pool. For buy-side repo participants, this access to liquidity is underpinned by capacity, risk management and efficiency — the three most important components of any repo service.

THE VIRTUOUS CIRCLE OF REPO CLEARING

While repo clearing is important for the industry, not all repo clearing services are the same. LCH is a unique financial infrastructure provider that allows you to benefit from an array of clearing services, across securities, rates, credit, equities and FX. Furthermore, as we operate from multiple locations and are in growing demand, we have the supply and quality of service that in turn generate more liquidity.

Volumes at LCH RepoClear have soared by more than 50% in the 10 years from 2010 to 2020. This is important for all repo participants, as both the concentration of available liquidity and the breadth of coverage are essential to providing participants with strong risk management and access to a range of cleared repo markets. The larger the netting pool, the greater the likelihood of a nettable trade and better price. With 14 debt markets in its netting pool, LCH RepoClear has a positive impact on capacity, which translates to better prices for buy-side clients.

OPEN FOR BUSINESS

Unlike a vertical exchange silo, LCH RepoClear is open and connected (see Figure 1). That means we operate how participants want, not the way we tell them to. This Open Access mentality drives us to be innovative, to partner with the market and to develop solutions that are primarily in the interests of participants.

At LCH RepoClear, this openness extends to our location, with services available in the UK and Paris, providing access across regulatory borders to a diverse, global membership, including our newest members in Luxembourg, Canada, Japan and Switzerland. LCH SA’s RepoClear service for Europe is a great example of this, demonstrating resilience by providing access to deep liquidity and margin stability during last year’s market stress.

LCH RepoClear’s clearing member network continues to expand, as does our innovative product offering, which has seen the growth of sponsored clearing and the addition of new products. And with both UK- and EU-based clearing houses, LCH RepoClear is uniquely positioned to continue delivering a seamless and diversified service for UK and European repo and cash bond markets with versatile trading and settlement optionality.

Participants looking to clear repo in the UK or Europe have choices, regardless of their market situation. But for those looking for access to the most liquidity, balance sheet netting opportunities, a predictable margin environment and an array of operational efficiencies, there is really only one option.

DISCLAIMER This article has been provided to you for informational purposes only and is intended as an overview of certain aspects of, or proposed changes to, services provided by LCH Limited (“LCH”). This document does not, and does not purport to, contain a detailed description of any aspect of an LCH service or any other matter set out in this document, and it has not been prepared for any specific person. This document does not, and does not seek to, constitute advice of any nature. You may not rely upon the contents of this document under any circumstance and should seek your own independent legal, investment, tax and other advice. The information contained in this document does not constitute a recommendation or offer with respect to any derivative contract, financial instrument, security or service. LCH makes no representation, warranty or guarantee (express or implied) that the contents of this document are accurate, complete or up-to-date, and LCH makes no commitment to offer any particular product or service. LCH shall have no liability for any losses, claims, demands, actions, proceedings, damages, costs or expenses arising out of, or in any way connected with, the information contained in this document, except that LCH accepts liability for personal injury or death caused by its negligence, for its fraud or wilful misrepresentation, and for any other liability which cannot be excluded by applicable law. LCH Limited is supervised by the Bank of England within the UK regulatory framework, registered as a derivatives clearing organisation with the U.S. Commodity Futures Trading Commission (“CFTC”) and recognised as a third-country CCP under Regulation (EU) No. 648/2012 of the European Parliament and of the Council of 4 July 2012 on OTC derivatives, central counterparties and trade repositories (“EMIR”). LCH SA is regulated and supervised in France by the Autorité des Marchés Financiers, the Autorité de Contrôle Prudentiel et de Résolution and the Banque de France, authorised as an E.U. CCP under EMIR, registered as a derivatives clearing organisation with the CFTC and as a clearing agency with the U.S. Securities and Exchange Commission. LCH Limited and LCH SA also hold licenses in other jurisdictions in which they offer their services. More information is available at www.lch.com. Copyright © LCH Limited 2021. All rights reserved. The information contained in this document is confidential. By reading this document, each recipient agrees to treat it in a confidential manner and will not, directly or indirectly, disclose or permit the disclosure of any information in this document to any other person (other than its regulators or professional advisers who have been informed of the confidential nature of the information) without the prior written consent of LCH.

Found this useful?

Take a complimentary trial of the FOW Marketing Intelligence Platform – the comprehensive source of news and analysis across the buy- and sell- side.

Gain access to:

- A single source of in-depth news, insight and analysis across Asset Management, Securities Finance, Custody, Fund Services and Derivatives

- Our interactive database, optimized to enable you to summarise data and build graphs outlining market activity

- Exclusive whitepapers, supplements and industry analysis curated and published by Futures & Options World

- Breaking news, daily and weekly alerts on the markets most relevant to you