Amundi’s Perrier eyes next opportunities

There can be little doubt who deserves the credit for Amundi. Yves Perrier was chief executive when the Paris-based firm was formed in January 2010 by the merger of Credit Agricole and Societe Generale’s investment arms.

He was chief exec when the firm went public on Euronext in November 2015 to become at that time the biggest listing in the exchange’s history. He oversaw the July 2017 acquisition of Pioneer Investments, which made Amundi the top European and a top ten global manager by assets, and he is still the chief executive today.

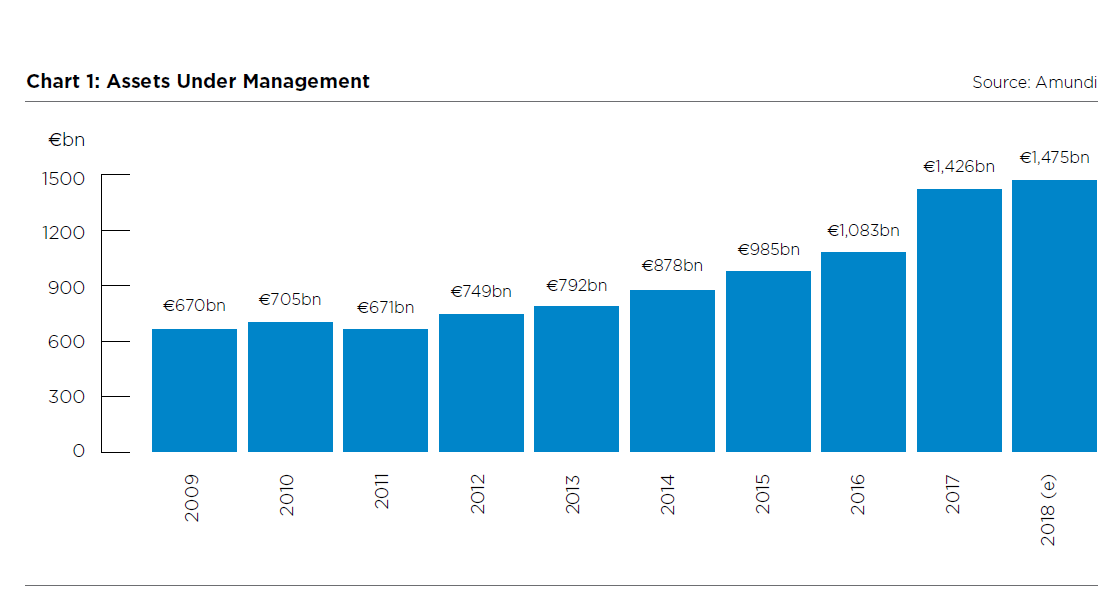

The firm’s growth in recent years has been impressive (see Chart 1). Amundi was managing just over €700bn of assets when it began in 2010 and now has more than double that number with €1,475bn of assets under management.

Amundi’s assets growth slowed in 2018 but this is to be expected in what has been a tough year for managers.

The French firm published at the end of October its financial results for the nine months to the end of September. Adjusted net income was up 11% on the previous year to €721m, partly due to the inclusion of Pioneer, operating expenses were down 4% to €1,005m and its cost/income ratio was 51.2%, which was 1.9% down on 2017 and among the lowest in the industry.

Perrier told Global Investor: “In a more difficult environment, Amundi’s results over the first nine months of 2018 are sharply up driven by robust business activity with €48.5bn in net inflows and by improved operational efficiency.”

Perrier continued: “The flows were mainly driven by medium to long term assets (assets excluding treasury product) and the international segment.”

Yves Perrier

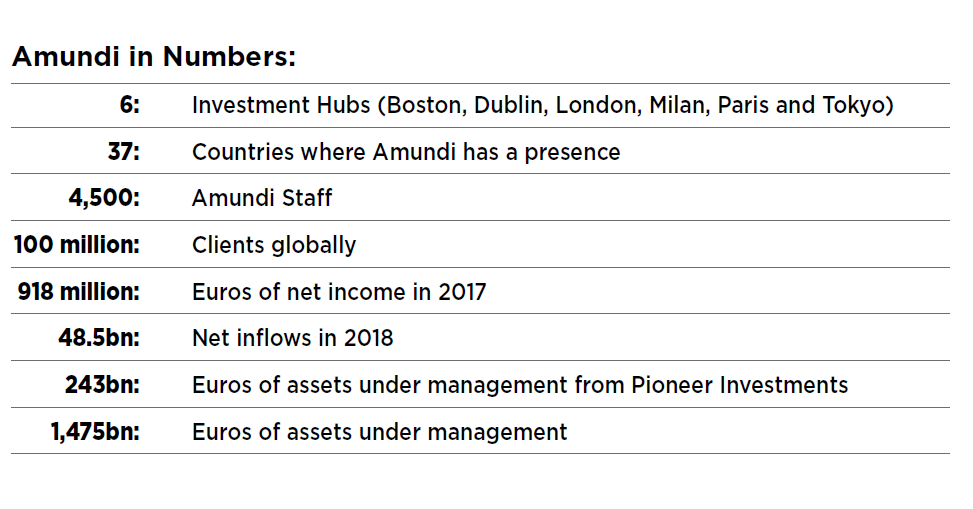

Amundi has six international investment hubs and a presence in some 37 countries which gives it nice regional diversification.

Perrier said: “These good performances reflect the strength of the Group’s business model, based on its business lines diversity (client segments, investment expertise and regions). This business model is further strengthened by the successful integration of Pioneer Investments.”

Pioneer, a US manager by birth more recently owned by Italy’s Unicredit, has boosted Amundi’s distribution and investment capabilities in North America, and enhanced its offering for Asian and Middle Eastern investors.

Looking ahead, the chief executive said: “Our primary focus remains in Europe and Asia. Indeed, the Eurozone is our natural home market, and we want to build-up a second domestic market in Asia.”

Four of Amundi’s six international investment hubs are in Europe (at least until the UK leaves the European Union). Dublin handles offshore business while London, Paris and Milan support clients in three of Europe’s top four economies.

Perrier continued: “We will consolidate our position as a reference partner in the retail segment through our savings solutions for networks in Europe: Unicredit in Italy, HVB in Germany and Bank Austria, and distributors in Europe and Asia for example. We will also accelerate our development in the institutional segment.”

Amundi’s other investment centres are Boston, the birthplace of Pioneer, and Tokyo. The Paris-based fund manager also has local investment centres in Hong Kong, Kuala Lumpur and Singapore as well as partnerships in Mumbai, Seoul and Shanghai.

Perrier said: “In Asia, joint ventures with large local retail banks, for example ABC in China and SBI in India, were the best way to address the retail market in China and India and they have been very successful. These regions are particularly dynamic as they benefit from the development of a new middle class.”

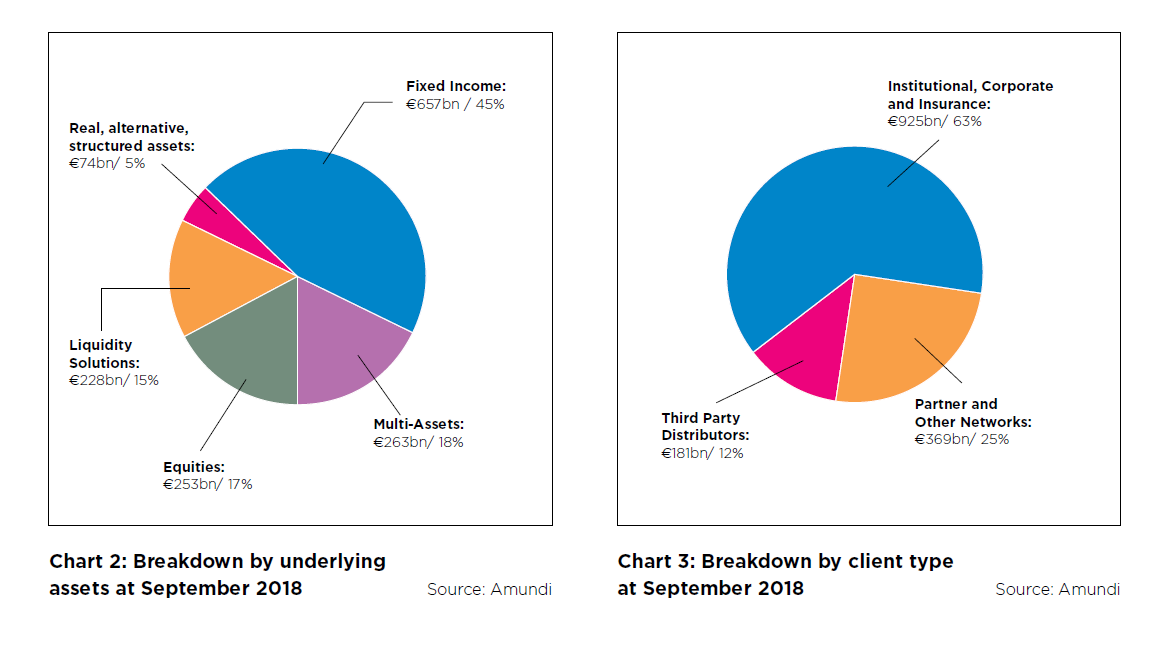

He added: “Our Asian subsidiaries, such as Singapore, HK, Taiwan and Japan, are a bridgehead to address other retail or institutional markets.” Amundi then has a strong international distribution network backed up by a mix of investment products (see Chart 2).

Some 45% of its assets under management is from fixed income strategies, 17% is from equities funds, 18% comes from multi-asset portfolios and 15% of income is from a line called liquidity solutions.

But Amundi is not immune to a trend that has dominated asset management in recent years, namely fee compression linked to the widespread adoption of

low cost passive funds.

Perrier said: “The entire financial sector is being challenged by pressures on margins and this trend is going to continue due to very low interest rates. This can be observed on the rate of mortgage loans, or on the returns of savings. The asset management industry is also being challenged by the development of passive management.”

The Amundi chief continued: “Europe is at an earlier stage than the US in terms of penetration rate of exchange-traded funds (ETFs) and passive management. However, the long term growth rates are quite similar between the two markets. We believe that passive will continue to grow in Europe at a higher pace than active management.”

But Perrier said he is not taking sides in this debate however: “We consider that both active and passive management will continue to coexist and prosper. Amundi’s strategy is to offer both active and passive products, and to continue to propose unbiased advice to its clients while benefitting from the development of passive segment.”

Perrier said the answers to the challenge of fee compression are building scale and finding new sources of income.

“Asset management is an industry of fixed costs, and consequently size generates benefits in terms of economies of scale, which can be reinvested to support growth and absorb margin pressure,” he said.

Tough market conditions have forced Amundi’s clients, such as pension or sovereign wealth funds, to re-assess their relationships with the firms that manage their money.

Perrier said: “Clients tend to reduce the numbers of providers of asset manager services, focusing on a few global leaders like Amundi complemented by the offer of some specialist players.”

But there is more than one way to bulk-up: “Achieving critical size is one of the responses to declining incomes. That is why we do therefore expect some consolidation in the industry,” said Perrier.

He continued: “Organic growth is the DNA of Amundi since its creation. In the meantime bolt-on acquisitions are possible, provided that the targeted acquisitions can accelerate Amundi’s development within the following three dimensions: reinforce Amundi’s product expertise (notably real assets, passive/ETF); broaden distribution channels; and expand geographic reach with a focus on Europe and Asia.”

Perrier added: “In any case, we will keep a highly disciplined approach, with requirements in line with past acquisitions: significant value creation through revenue and cost synergies; manageable execution and integration risk; and return on investment above 10% within three years.”

Another prong to Amundi’s strategy is product diversification, with ETFs, factor-based strategies and real assets among the priorities. Responsible

investing is also important.

Perrier told Global Investor: “One of Amundi key strengths is to be one of the very few players if not the only one to offer the full scope of Smart Beta and Factor Investing solutions, with all types of implementations including ETF, index funds and active funds.”

He added: “We have a long experience with our first active Smart Beta strategy being launched in 2007 and we were the first to launch a multifactor ETF in 2014 with Edhec Risk.”

Factor-based investing, or smart beta, has grown in popularity over recent years and is now evolving to include multi-factor strategies and fixed income factors.

Perrier said: “In today’s challenging environment, we believe that these strategies can be an appropriate answer for investors who want to mitigate risk in their portfolio for a more sustainable performance in the long-run.”

Factor-based strategies are resourceintensive however. Firms like Amundi have to invest in the best minds to create these strategies and these are not cheap given these academics are much in demand.

Perrier said: “In addition to standard or ready-to use strategies, the Smart Beta and Factor Investing platform leverages the group’s extensive research capabilities to develop fully customised solutions matching specific clients’ needs.”

He continued: “Over the past two years, we invested extensively with senior hires in the portfolio management and research teams, as well as in product development and innovation in order to accompany our clients growing interest. In parallel we extended our academic partnership with the EDHEC-Risk Institute, to cover factor investing in bond markets. Amundi manages today €23bn of assets under management (at end September 2018) and our ambition is to become the reference partner of investors in this field.”

Amundi has a relatively small allocation to real, alternative or structured assets. The asset manager has real assets worth €74bn, which is 5% of its total assets under management, according to the firm.

The manager and Preqin, the alternative investments expert, launched in June a comprehensive analysis of the alternative assets markets in Europe. The study uses data collected by Preqin since 2003 to give a view of the world’s second largest market (after North America) for alternative investments such as private equity, private debt, real estate, infrastructure and natural resources.

Pedro-Antonio Arias, global head of real and alternative Assets at Amundi, said in June: “It is no longer just European banks and governments providing funding for the real economy: insurance companies and pension schemes are also playing their part. The popularity of alternative investments among pension schemes and insurance

companies is well understood: the unconventional monetary policies developed in response to the global financial crisis had a significant impact on all asset classes.”

The report said the European alternatives investment industry passed €1.5 trillion in late 2017 and comprises over 5,000 investment firms managing assets for 2,800 investors. Arias continued: “Real assets are appealing to long-term investors for three reasons: they allow such investors to capture an illiquidity premium; they enhance income through a source of predictable returns; and they create diversification, as they have low correlation to traditional asset classes.”

Perrier then is committed to a strategy of regional and functional diversification backed up by financial performance targets for the period of 2018 to 2020.

Amundi charged itself in February 2018 with delivering total net inflows over the three years of €150bn (vs €120bn for 2016–2018) and an adjusted net income of more than €1.05bn (compared with €918m in 2017). The asset manager also restated its strategic objectives: a clientcentric organisational structure, both global and local; a policy of innovation to bring to customers a wide range of expertises; a robust infrastructure particularly in IT; and an entrepreneurial spirit.

Perrier has built in the past nine years a large, diverse asset management firm that rivals the world’s top investment firms in Europe and Asia. Amundi’s distribution is among the best in its peer group and it continues to invest heavily in new areas such as ETFs and sustainable strategies.

Pioneer has been digested in record time so the stage looks set for the next trade which will likely speak to one or more of Amundi’s ambitions in real assets, passive investments, Europe and Asia. Perrier has done well to get Amundi to where it is but his 2020 objectives suggest there is more work ahead.

Found this useful?

Take a complimentary trial of the FOW Marketing Intelligence Platform – the comprehensive source of news and analysis across the buy- and sell- side.

Gain access to:

- A single source of in-depth news, insight and analysis across Asset Management, Securities Finance, Custody, Fund Services and Derivatives

- Our interactive database, optimized to enable you to summarise data and build graphs outlining market activity

- Exclusive whitepapers, supplements and industry analysis curated and published by Futures & Options World

- Breaking news, daily and weekly alerts on the markets most relevant to you